Google Ad spend grew 11% in 2Q2022 - first growth since early 2021

Latest Tinuiti Digital Benchmark Report (July 2023) provides metrics on Google Ads and other online advertising platforms for the second calendar quarter of 2023 (April-May-June).

Key findings for Google Shopping, Performance Max and Text Ads:

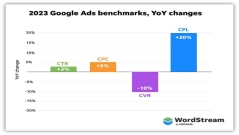

- Google search ad spend picked up as CPC deceleration reversed.

- Google Ad spend grew 11% in 2Q2023 - up from 9% in 1Q - the first acceleration in growth since early 2021.

- Google search CPCs were up by an average of 25% from 2019 levels, compared with +20% in 1Q2023..

- Average order value (AOV) from Google search was up a weak 1% vs 2Q2022, as inflation growth cooled. Slow AOV growth has limited sales-per-click growth and helped advertisers hold CPCs down and maintain a steady ROI from search ads.

- "Get Location Details" clicks returned to 2022 level in 2Q2023 after running significantly higher in 1Q, but were still +43% vs. 2Q2019.

- Although Google ended creation of new similar first-party audience segments, existing audiences still accounted for 12% of clicks in 2Q2023. Only Affinity and In-Market segments had higher traffic shares than Similar Audiences.

- Spend on Google text search ads was up 10% YOY in 2Q2023, compared to +9% in 1Q. Clicks held flat at 7% growth YOY, while CPC growth rose to 2% in 2Q2023 vs. 2% in Q1.

- Spend on Google Shopping/Performance Max campaigns grew 11% YOY in 2Q2023, up from 10% in Q1. Click growth was down slightly to 13% YOY, while CPC growth declined 2% YOY.

- Performance Max campaign adoption grew in 2Q2023 to 86% of advertisers running shopping listings, about +5% from 1Q.

- Video inventory on YouTube and display sources accounted for 2+% of Performance Max spend in 2Q2023, up only slightly from Q1.

- Mobile app share of non-search PMax impressions grew to 16% in 2Q2023, with the lion's share (45%) coming from non-Google web pages.

- YouTube ad spend grew by 9% YOY in 2Q2023, compared to 8% in Q1, while average CPM fell 18% YOY.

- Google Display inventory saw stronger CPM growth in 2Q2023, with Google Display Network registering just slightly negative growth vs. -5% in Q1, while Google DV360 placements saw CPM growth of 3% YOY vs. 10% decline in 1Q.

Data come from anonymized advertising programs managed by Tunuiti that have remained active and with consistent strategy, and account for an annual spend of more than $3B.

Comment: Inflation and interest rate increases by the Fed are still significant factors in what Google advertisers are paying for clicks. Both of these cut into discretionary consumer spending, and that cuts into Google's revenue from ads, which in turn causes Google to raise CPCs in order to keep cash flowing in. If you're reducing your ad spend in order to stay in business until the economy recovers, remember that Google Ads has been getting results for businesses consistently for a long time.

- David

- David

Comments on Google Ad spend grew 11% in 2Q2022 - first growth since early 2021